Microdramas represent the next evolution of storytelling: mobile-native, hyper-fragmented vertical series optimized for thumb-scrolling, instant hooks, and rapid emotional payoff. Episodes run 60–180 seconds with 50–100+ per season, built on relentless cliffhangers and compressed emotional archetypes — romance, betrayal, revenge, status fantasy. AI is accelerating the format globally by slashing costs and compressing iteration cycles from months to weeks.

The shift from long-form to mobile loops

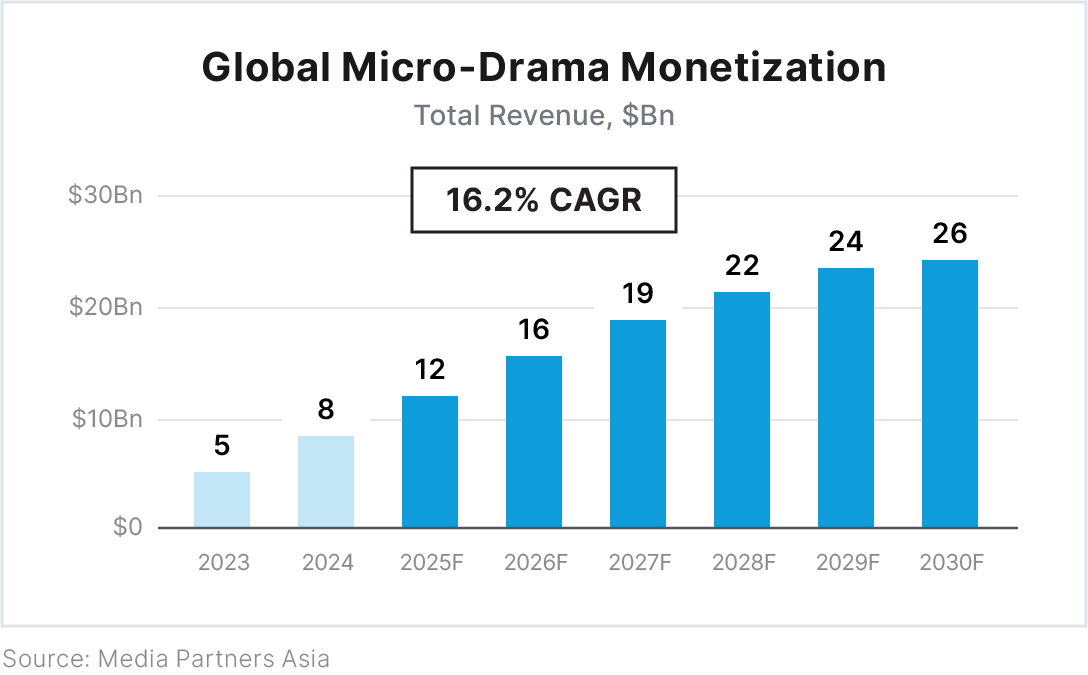

For years, scripted entertainment centered on prestige TV and bingeable seasons. Quibi failed by offering smaller TV instead of mobile-first design. Chinese platforms cracked the model first, treating microdramas like free-to-play games: free episodes to hook users, followed by paid unlocks. This flipped economics toward rapid testing and iteration. The model is now global, with ReelShort and DramaBox among the top-grossing entertainment apps and the U.S. as the second-largest market. Revenues reached roughly $11B in 2025 and are projected to exceed $14B in 2026 (with ~$3 billion coming from outside China1).

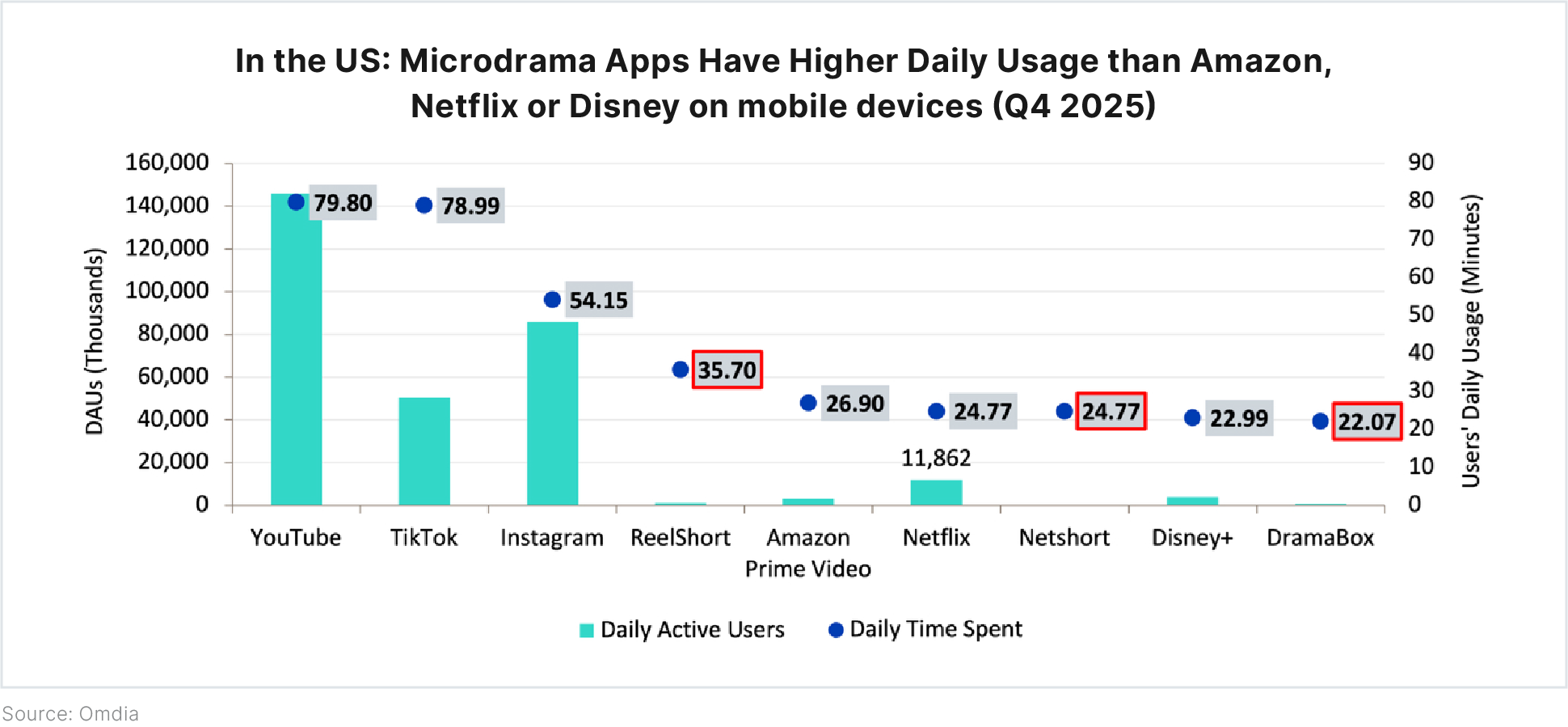

Microdrama apps win on engagement intensity. In the U.S. (Q4 2025), ReelShort averages 35.7 minutes per user per day — beating Netflix (24.8 min), Amazon Prime Video (26.9 min), and Disney+ (23.0 min). Idilio reaches ~45 minutes daily in Latin America.

AI changes production — taste becomes the bottleneck

Microdramas are structurally perfect for AI: small casts, limited sets, and pacing-first audiences. In China, AI has cut production costs by 80–90%, enabling hundreds of new titles monthly. But this shifts the constraint. The bottleneck is no longer production — it is taste. Many series hook early but collapse later because emotional arcs fail to sustain. As AI floods the market, taste, curation, and format design become the real advantage.

Players, monetization, and risks

Leaders in microdramas distribution include ReelShort and DramaBox, with a growing field of competitors like FlexTV, GoodShort, ShortMax, Holywater (My Drama), StoReel, and Idilio.tv.

The dominant monetization model across the industry mirrors mobile gaming: free episodes followed by paid unlocks via virtual coins. This drives strong ARPU but introduces real fragility. Heavy reliance on paid acquisition and aggressive cliffhanger gating risks rising customer acquisition costs (CAC), user fatigue, and potential regulatory pressure. We believe that a creator-first and culturally grounded approach offers a partial hedge against these risks by fostering higher organic retention and loyalty.

Idilio stands out as a prime example of taste and localized ecosystem advantage. The Colombian platform has achieved rapid traction in Latin America (1.5M+ downloads, strong monetization across Mexico, Colombia, US, Chile, and Spain) by prioritizing culturally resonant, original Spanish-language storytelling over dubbed imports. Its data-driven editorial system and Idilio Creators program, an open platform where writers retain 100% of monetization upside, blend telenovela heritage with AI production to deliver standout 45-minute daily engagement.

Players, monetization, and risks

AI removes the cost barrier but does not solve taste, retention, or differentiation. The winners will be those who execute the following strengths:

-

Taste-first localization as the primary competitive moat

-

Creator ecosystems as the main supply engine

-

Hybrid human + AI production at cultural scale

-

Shift from pay-per-episode friction to community + loyalty platforms

The shift is real, but the enduring advantage will come less from producing more and more from knowing what is actually worth producing through cultural taste, creator leverage, and responsible AI.

1) China still dominates (~83% of global revenue), while the U.S. has become the largest international market (projected ~$1.5 billion in 2026, or roughly 50% of non-China revenue).